In part I of keep more of your money in your family; choosing your process wisely I wrote about the well known traditional litigated court based divorce process and mediation. In this issue, I will cover Collaborative Divorce.

Collaborative divorce is an option you and your spouse should thoroughly explore before making any choice about divorce process. It is my belief that you and your spouse should first decide upon process before you ever hire an attorney. You can then match the right attorney to the right process. Just because they are, a divorce attorney does not mean they can be effective and efficient in all processes. In a collaborative divorce , a collaboratively trained attorney through the entire process represents each spouse.

A financial specialist helps couples sort out their financial issues including gathering all the financial data necessary for the divorce decree and presenting it to their respective attorneys in a format that helps attorneys review the numbers more efficiently. Contrast this with you and your spouse providing each of your attorneys the financial data, the two attorneys talking together about the financial data and then going back to you their client to discuss those conversations then going back again to the other attorney to discuss. Let me ask you on just this one basic step in the financial process, do you think you would keep more of your money in your family? Do you want to be paying two attorneys to do this financial data gathering or would you prefer to pay one financial specialist? A financial specialist is the one person who is in the best position to help you keep more of your financial resources in your family throughout the divorce process. They can save you taxes, come up with some creative options, and other ideas that allow both you and your spouse to create the best financial outcome for each of you given your existing resources.

In any divorce with minor children, a parenting plan is created and documented. In the collaborative divorce process, this is usually completed with a child specialist. This person helps parents articulate and document a well thought out plan to co-parent their children. The child specialist meets with the parents and often times meets with the children separately and then with everyone together. This level of attention to the family well-being is not found in other processes. You can of course work with two attorneys or a mediator to come up with a parenting time schedule and perhaps another piece or two of a well thought out plan. What you are not likely to get is a complete parenting plan that increases the likelihood of your children successfully navigating your divorce with you and your spouse.

Also available in the collaborative divorce process is a neutral divorce coach. The divorce coach helps spouses communicate effectively during the divorce process and come up with a plan for post divorce communication and relationship. This can lower conflict, which can decrease costs. If emotions run high at some point during the divorce process, a coach acts to ground you in the areas that are important to you. This enables both you and your spouse, to effectively communicate your needs, interests, and concerns all necessary to produce the higher-level outcome intended to last for a long time.

It is interesting to me that I often hear people say they are concerned about divorce costs when learning about collaborative divorce. Yet the collaborative divorce process minimizes attorney involvement since much of the work with the neutral financial specialist, neutral child specialist, and neutral divorce coach is completed without attorneys present. Attorneys usually are the highest paid professionals in any divorce process and most are not trained in financial issues, child and family systems, or other family relationship dynamics. What attorneys are trained in is the law. So imagine yourself utilizing a divorce process providing you with a menu of professional resources to help you and your family work with specialists in their respective fields and yet always have access to your own attorney who will be your advocate. Of the three processes discussed in this two issue article which do you think will allow you to keep more of your money in your family, traditional litigation, mediation, or collaborative divorce?

Remember to help you keep more of your money in your family choose your process wisely. In Part II of Keep More of Your Money in Your Family, I will write about choosing your attorney wisely.

Looking for some Twin Cities fun on a budget? Going from a duel income to a single income is not only difficult, but can bring on many emotions, especially if it leaves you feeling inadequate with providing for your children. There are so many low and no cost options out there that you don’t have to feel your children are missing out if you are on a single parent budget. Here are some of our favorites:

Looking for some Twin Cities fun on a budget? Going from a duel income to a single income is not only difficult, but can bring on many emotions, especially if it leaves you feeling inadequate with providing for your children. There are so many low and no cost options out there that you don’t have to feel your children are missing out if you are on a single parent budget. Here are some of our favorites:

- Como Zoo (free)

- Minneapolis Sculpture Garden (free)

- Walker Art Center (free admission Thursdays from 5-9pm)

- Minnesota History Center (free admission Tuesdays from 5-8pm)

- Fishing at many local community piers and parks (free)

- Minnehaha Falls (free)

- Three Rivers Parks District: Elm Creek Park Reserve, Lowery nature Center, Minnetonka Regional Park, etc. (free admission and many free activities and play equipment). Tip: make a list for a scavenger hunt before you go, kids LOVE scavenger hunts!

- Minnesota Children’s Museum (free admission the 3rd Sunday of each month)

- Outdoor concerts in the summer: Minneapolis Music in the Parks and St. Paul Music in the Parks, as well as many suburban concert series (free)

- Movies in the Park in Summer: many area options (free)

- Minnesota Landscape Arboretum (free admission every third Thursday of the month after 4:30 pm April through October)

- Farmer’s Markets: many area options, check your city and surrounding areas for dates and times. Tip: If you go close to the end of the day many vendors may have reduced their prices or are willing to negotiate on fresh produce. (free admission)

- Bike or walk the area trails. We are very blessed with many quality area trails like the Luce Line, Dakota Rail Regional Trail, etc. Tip: Another great place for a scavenger hunt!

- Local beaches in the summer – We are in the land of 10,000 lakes, there are so many options for free swimming and sand castle fun!

- Local art fairs, craft fairs, car shows, etc. Admission is typically free and it is so fun to walk around and look at everything.

Getting married sometimes can be expensive if you let it. Getting unmarried can be even more expensive if you and or your spouse allows it to get that way. In divorce, emotions are high and often contribute to higher levels of conflict. Conflict is expensive. Many divorcing couples want to know how they can keep more of their financial resources between themselves and in their family. After all the more that goes to pay for divorce costs means less for each spouse and for their children if they have children. In this upcoming series, I will write about some tips on how to keep more of your financial resources in your family. Here is the first tip:

Getting married sometimes can be expensive if you let it. Getting unmarried can be even more expensive if you and or your spouse allows it to get that way. In divorce, emotions are high and often contribute to higher levels of conflict. Conflict is expensive. Many divorcing couples want to know how they can keep more of their financial resources between themselves and in their family. After all the more that goes to pay for divorce costs means less for each spouse and for their children if they have children. In this upcoming series, I will write about some tips on how to keep more of your financial resources in your family. Here is the first tip:

- Choose your process wisely. Study your options and know what you and your spouse want. I ask divorcing clients what would need to happen in your divorce so you could look back three years from now and say this was a successful transition for your family and you. Paint that picture for me. Be honest with yourself.

- If you want a knock down drag out divorce, you know the Katie bar the door kind or I will show him/her, or I will make him/her pay, a more traditional litigation process certainly fits that bill. Moreover, that bill will be very expensive. On top of that, someone else, a judge, will be making decisions for you since you and your spouse are not able to reach agreements on your own. If you think, you are going to win and be the victor you have already lost because there are no winners in divorce. Most judges tend to think the best outcome if they have to decide your divorce is one when both spouses equally share the pain and both spouses are somewhat dissatisfied.

- You may consider mediation. Most people have heard about mediation. Mediation can be less expensive than a traditional court based process. Mediators however, are not able to provide legal advice. This is true even if the mediator is an attorney. Sometimes couples choose to have their own lawyers present at mediation sessions to overcome the no legal advice dilemma. Mediators, even if they are an attorney are not able to draft/prepare final divorce decree documents. If a mediator helps you reach agreements, you, and your spouse take those agreements to an attorney to draft the final documents and that attorney can only represent one of you, not both spouses. I always encourage my divorcing clients to each have their own attorney when reviewing any final documents resulting from mediation. You may run into one or both of the attorneys encouraging you not to accept the mediated agreements or parts of the agreements. In my practice, I recommend to clients attorneys that I know and have worked with, are settlement oriented, and not inclined to escalate conflict in an already mediated agreement. That is not to say there will not be some tweaks here and there because there always are and for good reason.

Allocating assets and liabilities between spouses is one of the financial pillars in any divorce. In my work as a financial neutral and also when working on behalf of an individual in a divorce the subject of credit card debt is often a topic that needs to be addressed. This is especially true when credit card balances are not paid in full each month.

The usual credit card ownership arrangements are joint or individual. There is another form of credit card ownership when one spouse is the primary account holder and the other spouse is an authorized user. In this situation, both spouses have a card on the same account issued in their individual name.

The thorny part of this is the primary account holder controls the decision-making authority relative to the account. The primary account holder can close the account. The authorized user generally is not able to close the account. However if the primary account holder defaults on the account the card issuer will seek payment from the authorized user. Does not seem quite right, does it? As an authorized user, you are unable to close the account yet if the primary account holder does not make payments, the authorized user can be liable for payment. What can you do to protect yourself?

Here are 5 suggestions:

- First, run a credit report on yourself from all three major credit-reporting agencies. These agencies include Equifax, TransUnion, and Experian. The best place to obtain this report is from www.annualcreditreport.com . Your report is free from this site and they will not solicit you for other purchases with one exception. Please note these reports do not include your credit score. You can obtain your score if you like for a nominal fee.

- Once you have the report from each of the three reporting agencies review all three reports carefully. The report will tell you if you own the card jointly, individually, or if you are an authorized user. This is a great time to verify the accuracy of all the data contained in the report.

- If you have a card issued in your name that for some reason does not appear on your credit report, call the issuer to determine your ownership status.

- If you are listed as an authorized user on any credit cards, call the issuer to determine how you can be removed.

- Let your attorney know you want any authorized user status clearly dealt with in your negotiations with your spouse. You do not want this thorny issue sneaking up on you down the road. In collaborative divorces, a well-trained financial neutral and the attorneys representing their clients are well aware of this issue.

The holiday season is when many people do a significant portion of their charitable giving for the year. Once you have decided which charitable organization to support and how much, you should also consider how to give that support. What I am getting at is that you can be charitable and tax-savvy by donating highly appreciated stock.

Donating a highly appreciated stock or mutual fund is a great strategy for getting rid of an investment that you have been holding because you do not want to pay the capital gains tax. The beauty of donating “in-kind” some or all of a security holding is that you get the full charitable deduction without paying the capital gains tax. “In-kind” means that the investment is not sold, but is transferred as-is to the charity instead. This way you do not have to pay the capital gains tax, because you did not sell the investment. The charity will likely sell the investment to meet their funding needs, but as a non-profit organization, they pay no tax on the sale.

The catch is that you have to have owned highly appreciated investment for more than one year. If you transfer an investment that you have owned for less than one year, you can only deduct your original cost in the investment and not the appreciation!

Of course this strategy is a bit more complicated than writing a check. You will need to obtain account information from the charity as to where to transfer the highly appreciated investment. You will then need to contact you investment broker and direct them to transfer the investment to the charity’s account. It is not difficult though; most charities are more than happy to help and it is something that investment brokers handle for their client on a regular basis.

The transfer has to occur by December 31st to qualify as a current year contribution. You cannot donate investments that have lost value and deduct their higher original cost. If your donation totals more than $250, the donation must be recorded – meaning that the charity must send you a written statement describing the donation and its value. You or your tax preparer will also need to fill out and include Form 8283 Noncash Charitable Contributions in your tax return, listing information about the charity and investment contributed.

Despite the extra work, donating highly appreciated stocks or mutual funds can be a win-win for you and the charity. This holiday season think about sharing some of your investment success with your favorite charity instead of with the IRS in April.

The holiday season is when many people do a significant portion of their charitable giving for the year. Once you have decided which charitable organization to support and how much, you should also consider how to give that support. What I am getting at is that you can be charitable and tax-savvy by donating highly appreciated stock.

Donating a highly appreciated stock or mutual fund is a great strategy for getting rid of an investment that you have been holding because you do not want to pay the capital gains tax. The beauty of donating “in-kind” some or all of a security holding is that you get the full charitable deduction without paying the capital gains tax. “In-kind” means that the investment is not sold, but is transferred as-is to the charity instead. This way you do not have to pay the capital gains tax, because you did not sell the investment. The charity will likely sell the investment to meet their funding needs, but as a non-profit organization, they pay no tax on the sale.

The catch is that you have to have owned highly appreciated investment for more than one year. If you transfer an investment that you have owned for less than one year, you can only deduct your original cost in the investment and not the appreciation!

Of course this strategy is a bit more complicated than writing a check. You will need to obtain account information from the charity as to where to transfer the highly appreciated investment. You will then need to contact you investment broker and direct them to transfer the investment to the charity’s account. It is not difficult though; most charities are more than happy to help and it is something that investment brokers handle for their client on a regular basis.

The transfer has to occur by December 31st to qualify as a current year contribution. You cannot donate investments that have lost value and deduct their higher original cost. If your donation totals more than $250, the donation must be recorded – meaning that the charity must send you a written statement describing the donation and its value. You or your tax preparer will also need to fill out and include Form 8283 Noncash Charitable Contributions in your tax return, listing information about the charity and investment contributed.

Despite the extra work, donating highly appreciated stocks or mutual funds can be a win-win for you and the charity. This holiday season think about sharing some of your investment success with your favorite charity instead of with the IRS in April.

As a neutral child specialist, I believe Collaborative Practice should be available to all families who want a child-focused, respectful, out-of-court divorce process. However, a critique often made of Collaborative Practice is how unaffordable it must be for families with limited financial resources. How could it be otherwise for a process that involves two attorneys and likely several neutral financial and/or mental health professionals?

Most of these critics are not aware that the Collaborative Law Institute has had ongoing Pro Bono/Low Bono Programs for over a decade. The goal of the current CLI Low Bono Committee is to provide very low cost but high quality services to clients who qualify, including the option of working with a full multidisciplinary team of divorce professionals.

We understand that financial hardship not only profoundly complicates day to day life but compounds the stress of getting unmarried. We realize that many parents who struggle through the massive amount of paperwork required for a do-it-yourself divorce eventually end up in court trying to sort out issues they hadn’t anticipated or didn’t fully understand at the time. We believe families in financial distress deserve a choice that will empower them to make their own decisions, but with the benefit of skillful professional support.

If you are in financial hardship and contemplating a divorce, we hope we can help. Go to the website for the Collaborative Law Institute of Minnesota and click the About Us tab at the top right of the homepage. Next, click on No Cost or Low Cost (Pro Bono) Programs to find the online application for low bono Collaborative services. Applications are screened for eligibility by the Low Bono Committee, but are otherwise completely confidential. If you are interested, we hope to hear from you!

Most of these critics are not aware that the Collaborative Law Institute has had ongoing Pro Bono/Low Bono Programs for over a decade. The goal of the current CLI Low Bono Committee is to provide very low cost but high quality services to clients who qualify, including the option of working with a full multidisciplinary team of divorce professionals.

We understand that financial hardship not only profoundly complicates day to day life but compounds the stress of getting unmarried. We realize that many parents who struggle through the massive amount of paperwork required for a do-it-yourself divorce eventually end up in court trying to sort out issues they hadn’t anticipated or didn’t fully understand at the time. We believe families in financial distress deserve a choice that will empower them to make their own decisions, but with the benefit of skillful professional support.

If you are in financial hardship and contemplating a divorce, we hope we can help. Go to the website for the Collaborative Law Institute of Minnesota and click the About Us tab at the top right of the homepage. Next, click on No Cost or Low Cost (Pro Bono) Programs to find the online application for low bono Collaborative services. Applications are screened for eligibility by the Low Bono Committee, but are otherwise completely confidential. If you are interested, we hope to hear from you!

Most of these critics are not aware that the Collaborative Law Institute has had ongoing Pro Bono/Low Bono Programs for over a decade. The goal of the current CLI Low Bono Committee is to provide very low cost but high quality services to clients who qualify, including the option of working with a full multidisciplinary team of divorce professionals.

We understand that financial hardship not only profoundly complicates day to day life but compounds the stress of getting unmarried. We realize that many parents who struggle through the massive amount of paperwork required for a do-it-yourself divorce eventually end up in court trying to sort out issues they hadn’t anticipated or didn’t fully understand at the time. We believe families in financial distress deserve a choice that will empower them to make their own decisions, but with the benefit of skillful professional support.

If you are in financial hardship and contemplating a divorce, we hope we can help. Go to the website for the Collaborative Law Institute of Minnesota and click the About Us tab at the top right of the homepage. Next, click on No Cost or Low Cost (Pro Bono) Programs to find the online application for low bono Collaborative services. Applications are screened for eligibility by the Low Bono Committee, but are otherwise completely confidential. If you are interested, we hope to hear from you!  Parents with children who attend college get to take part in the annual ritual of filling out the Free Application for Student Aid (FAFSA). The FAFSA can be nearly as difficult as Calculus 101, but unlike calculus this math, can have real implications to your life and financial situation. If you are divorced with a child heading off to college, below are some things that you should know about FAFSA and student financial aid.

The custodial parent is responsible for filling out FAFSA and it is only their financial and household situation that are reported on the FAFSA. This can have important implications for determining eligibility for aid and for calculating the Expected Family Contribution (EFC) to the student’s college expenses. Determination of the custodial parent follows the criteria below, in descending order of importance:

Parents with children who attend college get to take part in the annual ritual of filling out the Free Application for Student Aid (FAFSA). The FAFSA can be nearly as difficult as Calculus 101, but unlike calculus this math, can have real implications to your life and financial situation. If you are divorced with a child heading off to college, below are some things that you should know about FAFSA and student financial aid.

The custodial parent is responsible for filling out FAFSA and it is only their financial and household situation that are reported on the FAFSA. This can have important implications for determining eligibility for aid and for calculating the Expected Family Contribution (EFC) to the student’s college expenses. Determination of the custodial parent follows the criteria below, in descending order of importance:

- The Custodial parent is considered the parent with whom the child lived the majority of the time over the 12 months prior to completion of the FAFSA (not the previous calendar year).

- If custody time is equally split, the parent providing more financial support over the past 12 months.

- The parent that provides more than half of support now and will continue to do so in the future.

- The above are the primary criteria, but other criteria used to substantiate the above include who has legal custody, claimed the student on their tax return or has the higher income.

- Investment and property liquidations

- Retirement plan divisions that include a distribution to the parent

- College expense payments required by the divorce decree will be included in the student’s income.

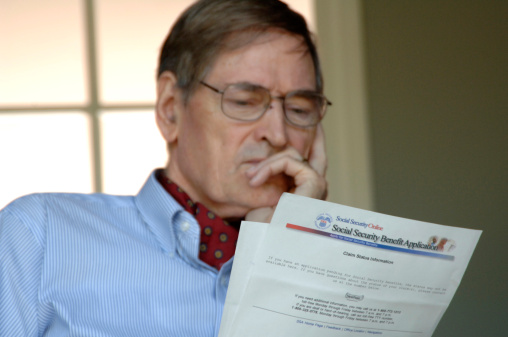

When contemplating the pros and cons of getting divorced, I doubt anyone ever puts in the pros column “easier to claim Social Security Spousal Benefits”. Some people may not even realize that they can get Social Security spousal benefits based on their ex-spouse’s work record. Below are some of the basics of claiming spousal benefits after divorce.

Social Security spousal benefits, whether married or divorced, are calculated to be 50% of the spouse’s Primary Insurance Amount (PIA) at their Full Retirement Age (FRA). That is 50% of the benefit amount the ex-spouse would receive if they applied for benefits sometime after their 66th birthday (currently). In order to be eligible to claim spousal benefits on an ex-spouse’s work record, one has to be over age 62 and so does the ex-spouse. The marriage has to have lasted at least 10 years and one has to be divorced for 2 years. Finally, one cannot have remarried and it doesn’t matter if the ex-spouse has remarried.

The advantage of being divorced and claiming spousal benefits is that the ex-spouse does not need to be receiving benefits. Married couples have to undertake some complicated paperwork machinations if one spouse wants to claim spousal benefits while the other spouse continues to work. A divorced person doesn’t even need to interact with their ex-spouse to claim benefits based on that person’s work record. One has to provide the ex-spouse’s social security number, a marriage certificate and a divorce decree to claim spousal benefits.

The ramifications of claiming spousal benefits prior to your own FRA should be thoroughly understood before applying early. The same reductions in benefits that affect anyone applying for benefits before their FRA also apply to spousal benefits. For example, an ex-spouse claiming spousal benefits as early as possible – age 62, will have their benefit reduced by approximately 25%. Instead of receiving 50% of their ex-spouse’s PIA, they will receive approximately 35% of that benefit.

Another important consequence of applying before one’s own FRA is that social security actually awards benefits based on one’s own work record. If the spousal benefit is greater than one’s own benefit, social security adds the difference to one’s own benefit instead of solely awarding spousal benefits. There is a misconception that one can claim spousal benefits prior to their FRA, let their own benefits continue to grow and switch to their own benefit later. Since social security is actually awarding one’s own benefit for a claim prior FRA, this strategy not possible.

The good news is that one can do the switching strategy after their FRA. We have helped divorced working women who have reached full retirement age claim spousal benefits based their ex-husband’s work record. They can receive spousal benefits beginning at their FRA until age 70, while their own benefits continue to grow. By delaying claiming their own benefits until age 70, social security automatically increases their benefits 8% for each year they delay past their FRA. Continuing to work may increase their benefit even further.

An additional advantage of waiting to claim benefits until after one’s FRA is that benefits will not be reduced if still working. Anyone claiming benefits prior to their FRA and earning over $15,000 in W-2 income from a job will likely see their benefits reduced. After one’s FRA, one can work without a reduction in benefit and as already mentioned may see their benefit increase.

Social Security is a complex program, so whether divorced or married, it is best to meet with a financial advisor to discuss when to take social security before applying for benefits.

When contemplating the pros and cons of getting divorced, I doubt anyone ever puts in the pros column “easier to claim Social Security Spousal Benefits”. Some people may not even realize that they can get Social Security spousal benefits based on their ex-spouse’s work record. Below are some of the basics of claiming spousal benefits after divorce.

Social Security spousal benefits, whether married or divorced, are calculated to be 50% of the spouse’s Primary Insurance Amount (PIA) at their Full Retirement Age (FRA). That is 50% of the benefit amount the ex-spouse would receive if they applied for benefits sometime after their 66th birthday (currently). In order to be eligible to claim spousal benefits on an ex-spouse’s work record, one has to be over age 62 and so does the ex-spouse. The marriage has to have lasted at least 10 years and one has to be divorced for 2 years. Finally, one cannot have remarried and it doesn’t matter if the ex-spouse has remarried.

The advantage of being divorced and claiming spousal benefits is that the ex-spouse does not need to be receiving benefits. Married couples have to undertake some complicated paperwork machinations if one spouse wants to claim spousal benefits while the other spouse continues to work. A divorced person doesn’t even need to interact with their ex-spouse to claim benefits based on that person’s work record. One has to provide the ex-spouse’s social security number, a marriage certificate and a divorce decree to claim spousal benefits.

The ramifications of claiming spousal benefits prior to your own FRA should be thoroughly understood before applying early. The same reductions in benefits that affect anyone applying for benefits before their FRA also apply to spousal benefits. For example, an ex-spouse claiming spousal benefits as early as possible – age 62, will have their benefit reduced by approximately 25%. Instead of receiving 50% of their ex-spouse’s PIA, they will receive approximately 35% of that benefit.

Another important consequence of applying before one’s own FRA is that social security actually awards benefits based on one’s own work record. If the spousal benefit is greater than one’s own benefit, social security adds the difference to one’s own benefit instead of solely awarding spousal benefits. There is a misconception that one can claim spousal benefits prior to their FRA, let their own benefits continue to grow and switch to their own benefit later. Since social security is actually awarding one’s own benefit for a claim prior FRA, this strategy not possible.

The good news is that one can do the switching strategy after their FRA. We have helped divorced working women who have reached full retirement age claim spousal benefits based their ex-husband’s work record. They can receive spousal benefits beginning at their FRA until age 70, while their own benefits continue to grow. By delaying claiming their own benefits until age 70, social security automatically increases their benefits 8% for each year they delay past their FRA. Continuing to work may increase their benefit even further.

An additional advantage of waiting to claim benefits until after one’s FRA is that benefits will not be reduced if still working. Anyone claiming benefits prior to their FRA and earning over $15,000 in W-2 income from a job will likely see their benefits reduced. After one’s FRA, one can work without a reduction in benefit and as already mentioned may see their benefit increase.

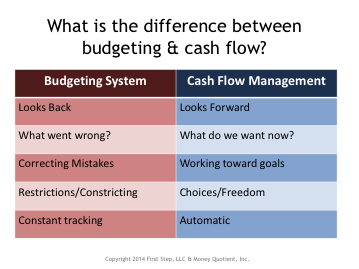

Social Security is a complex program, so whether divorced or married, it is best to meet with a financial advisor to discuss when to take social security before applying for benefits.  I teach a cash flow planning course throughout the metro area. One of the ways I begin, is by asking everyone to tell me the first word that comes to mind when they hear the word budget? Often it is a negative type of word like restricting, confining, or boring. When I ask a similar question about cash flow, common responses are future and choice. The chart below illustrates some of those differences.

I teach a cash flow planning course throughout the metro area. One of the ways I begin, is by asking everyone to tell me the first word that comes to mind when they hear the word budget? Often it is a negative type of word like restricting, confining, or boring. When I ask a similar question about cash flow, common responses are future and choice. The chart below illustrates some of those differences.

Money is one of those issues often cited as a reason for divorce. I would offer that money itself does not cause divorce. How spouses handle money differently and an inability to recognize their different money personalities and learn effective ways to work through those differences can lead to divorce or at least cause significant strain in a marriage.

Establishing reasonable and necessary future living expenses post-divorce is one of the two pillars of any divorce process. Both spouses will need to establish their own living expenses independently of one another. If money was a source of conflict in the marriage, imagine the conflict that exists during the divorce process. The reality is the money conflict can and often does escalate in divorce. In my work as a financial neutral, financial mediator, and financial planner, I work with you and your spouse to help you focus on your future.

One approach to creating a future oriented cash flow plan for your post-divorce life is to add up all of your expenses necessary for your basic living needs. This would include things like housing, food, clothing, and medical care to name a few. If you are familiar with Maslow’s hierarchy of needs, this would be the lower level (safety and security) in the hierarchy. Keep in mind that at this basic level food does not include dining out. Clothing does not include upscale designer clothing. Items in this safety and security level are for basic needs.

After taking care of basic needs you can then address expenses that you have total control and choice over such as dining out, entertainment, cash spending money, gifts, personal care, etc.

Finally, you may want to consider future goals and needs like retirement, creating an emergency savings plan, a different automobile, or an education.

Think of separating these expenses into three different categories. I ask my clients to visualize these as three distinct buckets. The buckets are one for basic needs, two control and choices, and three future needs and wants. It is important to recognize that during and after the divorce, you may need to at least temporarily forgo some if not all of the future needs and wants, and substantially minimize the control and choice buckets due to the initial financial strain of divorce.

It is equally important to recognize this time-period does not necessarily last forever. Incomes can and do increase over time and some expenses such as child-care reduce and ultimately disappear at some point.

A well-developed future oriented cash flow plan can give you the peace of mind to know you will be financially secure. It can give you the opportunity to choose what is important to you about money, prioritize your goals, and create a solid model and roadmap for your life ahead. A financial neutral in collaborative divorce process will help you create this type of plan.

A short three-minute video on the history of cash flow and money management is available by clicking here.

Money is one of those issues often cited as a reason for divorce. I would offer that money itself does not cause divorce. How spouses handle money differently and an inability to recognize their different money personalities and learn effective ways to work through those differences can lead to divorce or at least cause significant strain in a marriage.

Establishing reasonable and necessary future living expenses post-divorce is one of the two pillars of any divorce process. Both spouses will need to establish their own living expenses independently of one another. If money was a source of conflict in the marriage, imagine the conflict that exists during the divorce process. The reality is the money conflict can and often does escalate in divorce. In my work as a financial neutral, financial mediator, and financial planner, I work with you and your spouse to help you focus on your future.

One approach to creating a future oriented cash flow plan for your post-divorce life is to add up all of your expenses necessary for your basic living needs. This would include things like housing, food, clothing, and medical care to name a few. If you are familiar with Maslow’s hierarchy of needs, this would be the lower level (safety and security) in the hierarchy. Keep in mind that at this basic level food does not include dining out. Clothing does not include upscale designer clothing. Items in this safety and security level are for basic needs.

After taking care of basic needs you can then address expenses that you have total control and choice over such as dining out, entertainment, cash spending money, gifts, personal care, etc.

Finally, you may want to consider future goals and needs like retirement, creating an emergency savings plan, a different automobile, or an education.

Think of separating these expenses into three different categories. I ask my clients to visualize these as three distinct buckets. The buckets are one for basic needs, two control and choices, and three future needs and wants. It is important to recognize that during and after the divorce, you may need to at least temporarily forgo some if not all of the future needs and wants, and substantially minimize the control and choice buckets due to the initial financial strain of divorce.

It is equally important to recognize this time-period does not necessarily last forever. Incomes can and do increase over time and some expenses such as child-care reduce and ultimately disappear at some point.

A well-developed future oriented cash flow plan can give you the peace of mind to know you will be financially secure. It can give you the opportunity to choose what is important to you about money, prioritize your goals, and create a solid model and roadmap for your life ahead. A financial neutral in collaborative divorce process will help you create this type of plan.

A short three-minute video on the history of cash flow and money management is available by clicking here.

At first glance, you might think that beginning social security benefits at age 62 versus waiting until your full retirement age (FRA – currently age 66) sounds like a pretty good deal. You receive four more years of benefits and won’t have to withdraw as much from your savings as you would if you waited until your FRA. By not taking money out of your savings, the money can grow more than it would if it were relied upon to cover all living expenses.

Those arguments have some merit, but probably not as much as most might think. It may indeed make sense in some situations to begin benefits at 62, particularly for someone with serious health issues. However, for anyone expecting to live past their mid-70’s, the numbers tell a different story.

As an example, consider two 62-year olds (Ms. Early & Ms. Normal) who will both receive a primary insurance amount (PIA) of $2,200 per month at their FRA. Ms. Early opts to receive benefits at age 62 and accepts that she will only receive 75% of her PIA, or $1,650 per month. Ms. Normal decides to wait until her FRA (age 66) to receive her PIA of $2,200. Ms. Early is happy with her decision to start at 62 because she will have received $79,200 in cumulative benefits even before Ms. Normal receives her first benefit payment. When Ms. Normal begins receiving benefits, she receives $550 per month more than Ms. Early, thus Ms. Normal’s cumulative benefit grow faster than Ms. Early’s. At age 77, Ms. Normal’s cumulative benefits will overtake Ms. Early’s. If Ms. Early and Ms. Normal both pass away at age 87, Ms. Normal’s cumulative benefits will have exceeded Ms. Early’s benefit by $66,000.

Over 20 years, $66,000 ($3,300/year) may or may not seem like a lot, but one important detail was left out of the above example for simplicity. Social Security benefits are subject to an annual cost-of-living adjustment (COLA – a percentage increase to a benefit) to keep pace with inflation. The reality is that Ms. Early and Ms. Normal will both receive the same COLA percentage, but they will receive different dollar amounts due to their different benefit amounts. Since Ms. Normal’s benefit is greater than Ms. Early’s benefit, her COLA increase will be greater, causing the difference in their benefits to increase over time as well. If one assumes a 2% annual COLA, the monthly benefit difference grows from $550/month ($1,650 at 62 vs. $2,200 at 66) to $907/month at age 87 ($2,707 for Ms. Early vs. $3,909 for Ms. Normal). Using the 2% annual growth scenario, Ms. Normal’s cumulative benefits overtake Ms. Early’s a year earlier (age 76) and her cumulative benefit will exceed Ms. Early’s by $113,417 at age 87!

As with all annuity cash flow streams, the optimal time to start receiving benefits depends on the length of the time the benefit will be received. In other words, if you knew when you were going to die, it would really help determine when you should start taking benefits! As the examples above illustrates, Ms. Early would have been better off starting at age 62 if she knew she was going to die in her mid-70’s. But, the mathematics of longevity side with Ms. Normal because if Ms. Normal is alive at 65, Social Security’s own studies show that she has a 71% chance of living to age 80, a 53% chance of living to 85 and a 30% chance that she will live to 90.

It is unfortunate that the likelihood of living longer than one expects, and the cost of starting social security early, is not fully appreciated by most people who start their benefit at age 62. If they realized that they had a good chance of living to 90, and that by receiving benefits at 62 they were short-changing themselves of $147,219 in benefits, they might have continued to work a bit longer.

At first glance, you might think that beginning social security benefits at age 62 versus waiting until your full retirement age (FRA – currently age 66) sounds like a pretty good deal. You receive four more years of benefits and won’t have to withdraw as much from your savings as you would if you waited until your FRA. By not taking money out of your savings, the money can grow more than it would if it were relied upon to cover all living expenses.

Those arguments have some merit, but probably not as much as most might think. It may indeed make sense in some situations to begin benefits at 62, particularly for someone with serious health issues. However, for anyone expecting to live past their mid-70’s, the numbers tell a different story.

As an example, consider two 62-year olds (Ms. Early & Ms. Normal) who will both receive a primary insurance amount (PIA) of $2,200 per month at their FRA. Ms. Early opts to receive benefits at age 62 and accepts that she will only receive 75% of her PIA, or $1,650 per month. Ms. Normal decides to wait until her FRA (age 66) to receive her PIA of $2,200. Ms. Early is happy with her decision to start at 62 because she will have received $79,200 in cumulative benefits even before Ms. Normal receives her first benefit payment. When Ms. Normal begins receiving benefits, she receives $550 per month more than Ms. Early, thus Ms. Normal’s cumulative benefit grow faster than Ms. Early’s. At age 77, Ms. Normal’s cumulative benefits will overtake Ms. Early’s. If Ms. Early and Ms. Normal both pass away at age 87, Ms. Normal’s cumulative benefits will have exceeded Ms. Early’s benefit by $66,000.

Over 20 years, $66,000 ($3,300/year) may or may not seem like a lot, but one important detail was left out of the above example for simplicity. Social Security benefits are subject to an annual cost-of-living adjustment (COLA – a percentage increase to a benefit) to keep pace with inflation. The reality is that Ms. Early and Ms. Normal will both receive the same COLA percentage, but they will receive different dollar amounts due to their different benefit amounts. Since Ms. Normal’s benefit is greater than Ms. Early’s benefit, her COLA increase will be greater, causing the difference in their benefits to increase over time as well. If one assumes a 2% annual COLA, the monthly benefit difference grows from $550/month ($1,650 at 62 vs. $2,200 at 66) to $907/month at age 87 ($2,707 for Ms. Early vs. $3,909 for Ms. Normal). Using the 2% annual growth scenario, Ms. Normal’s cumulative benefits overtake Ms. Early’s a year earlier (age 76) and her cumulative benefit will exceed Ms. Early’s by $113,417 at age 87!

As with all annuity cash flow streams, the optimal time to start receiving benefits depends on the length of the time the benefit will be received. In other words, if you knew when you were going to die, it would really help determine when you should start taking benefits! As the examples above illustrates, Ms. Early would have been better off starting at age 62 if she knew she was going to die in her mid-70’s. But, the mathematics of longevity side with Ms. Normal because if Ms. Normal is alive at 65, Social Security’s own studies show that she has a 71% chance of living to age 80, a 53% chance of living to 85 and a 30% chance that she will live to 90.

It is unfortunate that the likelihood of living longer than one expects, and the cost of starting social security early, is not fully appreciated by most people who start their benefit at age 62. If they realized that they had a good chance of living to 90, and that by receiving benefits at 62 they were short-changing themselves of $147,219 in benefits, they might have continued to work a bit longer.