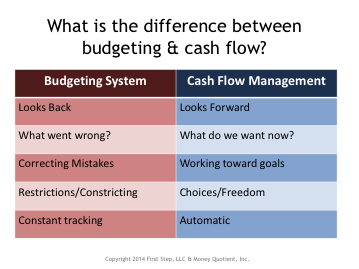

I teach a cash flow planning course throughout the metro area. One of the ways I begin, is by asking everyone to tell me the first word that comes to mind when they hear the word budget? Often it is a negative type of word like restricting, confining, or boring. When I ask a similar question about cash flow, common responses are future and choice. The chart below illustrates some of those differences.

Money is one of those issues often cited as a reason for divorce. I would offer that money itself does not cause divorce. How spouses handle money differently and an inability to recognize their different money personalities and learn effective ways to work through those differences can lead to divorce or at least cause significant strain in a marriage.

Establishing reasonable and necessary future living expenses post-divorce is one of the two pillars of any

divorce process. Both spouses will need to establish their own living expenses independently of one another. If money was a source of conflict in the marriage, imagine the conflict that exists during the divorce process. The reality is the money conflict can and often does escalate in divorce. In my work as a

financial neutral, financial mediator, and financial planner, I work with you and your spouse to help you focus on your future.

One approach to creating a future oriented cash flow plan for your post-divorce life is to add up all of your expenses necessary for your basic living needs. This would include things like housing, food, clothing, and medical care to name a few. If you are familiar with Maslow’s hierarchy of needs, this would be the lower level (safety and security) in the hierarchy. Keep in mind that at this basic level food does not include dining out. Clothing does not include upscale designer clothing. Items in this safety and security level are for basic needs.

After taking care of basic needs you can then address expenses that you have total control and choice over such as dining out, entertainment, cash spending money, gifts, personal care, etc.

Finally, you may want to consider future goals and needs like retirement, creating an emergency savings plan, a different automobile, or an education.

Think of separating these expenses into three different categories. I ask my clients to visualize these as three distinct buckets. The buckets are one for basic needs, two control and choices, and three future needs and wants. It is important to recognize that during and after the divorce, you may need to at least temporarily forgo some if not all of the future needs and wants, and substantially minimize the control and choice buckets due to the initial financial strain of divorce.

It is equally important to recognize this time-period does not necessarily last forever. Incomes can and do increase over time and some expenses such as child-care reduce and ultimately disappear at some point.

A well-developed future oriented cash flow plan can give you the peace of mind to know you will be financially secure. It can give you the opportunity to choose what is important to you about money, prioritize your goals, and create a solid model and roadmap for your life ahead. A financial neutral in

collaborative divorce process will help you create this type of plan.

A short three-minute video on the history of cash flow and money management is available by clicking

here.

More Collaborative Law Posts